Phillip Reese

Kirk Vartan pays greater than $2,000 a month for a high-deductible medical health insurance plan from Blue Shield on Covered California, the state’s Affordable Care Act market. He may have chosen a less expensive plan from a distinct supplier, however he wished one that features his spouse’s physician.

“It’s for the two of us, and we’re not sick,” stated Vartan, common supervisor at A Slice of New York pizza retailers within the Bay Area cities of San Jose and Sunnyvale. “It’s ridiculous.”

Vartan, who’s in his late 50s, is one in every of hundreds of thousands of Californians struggling to maintain up with medical health insurance premiums ballooning sooner than inflation.

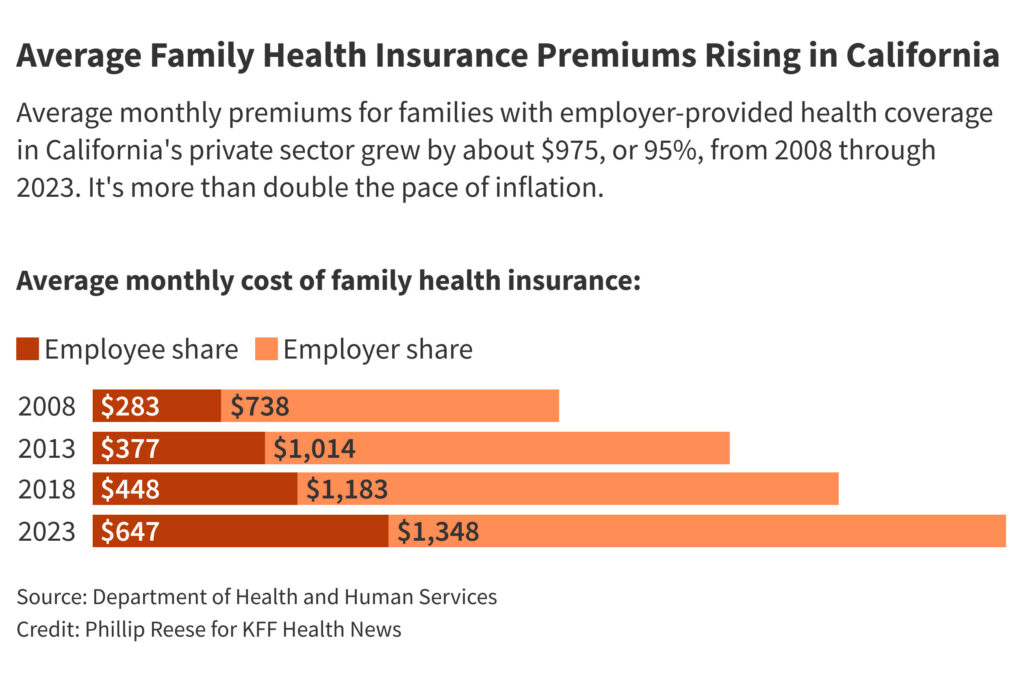

Average month-to-month premiums for households with employer-provided well being protection in California’s non-public sector almost doubled during the last 15 years, from simply over $1,000 in 2008 to virtually $2,000 in 2023, a KFF Health News evaluation of federal data shows. That’s greater than twice the speed of inflation. Also, workers have needed to take up a rising share of the fee.

The spike is just not confined to California. Average premiums for households with employer-provided well being protection grew as quick nationwide as they did in California from 2008 by 2023, federal data shows. Premiums continued to grow rapidly in 2024, in keeping with KFF.

Small-business teams warn that, for staff whose employers don’t present protection, the issue may worsen if Congress doesn’t lengthen enhanced federal subsidies that make medical health insurance extra reasonably priced on particular person markets reminiscent of Covered California, the general public market that insures greater than 1.9 million Californians.

Premiums on Covered California have grown about 25% since 2022, roughly double the tempo of inflation. But the alternate helps almost 90% of enrollees mitigate excessive prices by providing state and federal subsidies based on income, with many households paying little or nothing.

Rising premiums even have hit authorities staff — and taxpayers. Premiums at CalPERS, which gives insurance coverage to greater than 1.5 million of California’s lively and retired public workers and members of the family, have risen about 31% since 2022. Public employers pay a part of the price of premiums as negotiated with labor unions; staff pay the remaining.

“Insurance premiums have been going up faster than wages over the last 20 years,” stated Miranda Dietz, a researcher on the University of California-Berkeley Labor Center who focuses on medical health insurance. “Especially in the last couple of years, those premium increases have been pretty dramatic.”

Dietz stated rising hospital costs are largely responsible. Consumer prices for hospitals and nursing houses rose about 88% from 2009 by 2024, roughly double the general inflation charge, in keeping with knowledge from the Department of Labor. The rising price of administering America’s large well being care system has additionally pushed premiums greater, she stated.

Insurance corporations stay extremely worthwhile, however their gross margins — the quantity by which premium revenue exceeds claims prices — had been pretty regular throughout the previous few years, KFF research shows. Under federal guidelines, insurers must spend a minimum proportion of premiums on medical care.

Rising insurance coverage prices are reducing deeper into household incomes and squeezing small companies.

The common annual price of household medical health insurance provided by non-public sector corporations was about $24,000, or roughly $2,000 a month, in California throughout 2023, in keeping with the U.S. Department of Health and Human Services. Employers paid, on common, about two-thirds of the invoice, with staff paying the remaining third, about $650 a month. Workers’ share of premiums has grown sooner in California than in the remainder of the nation.

Many small-business staff whose employers don’t provide well being care flip to Covered California. During the final three a long time, the share of companies nationwide with 10 to 24 staff providing medical health insurance fell from 65% to 52%, in keeping with the Employee Benefit Research Institute. Coverage fell from 34% to 23% amongst companies with fewer than 10 workers.

“When an employee of a small business isn’t able to access health insurance with their employer, they’re more likely to leave that employer,” stated Bianca Blomquist, California director for Small Business Majority, an advocacy group representing greater than 85,000 small companies throughout America.

Kirk Vartan stated his pizza store employs about 25 folks and operates as a employee cooperative — a enterprise owned by its staff. The small enterprise lacks negotiating energy to demand reductions from insurance coverage corporations to cowl its staff. The greatest the store may do, he stated, had been costly plans that may make it exhausting for the cooperative to function. And these plans wouldn’t provide as a lot protection as staff may discover for themselves by Covered California.

“It was a lose-lose all the way around,” he stated.

Mark Seelig, a spokesperson for Blue Shield of California, stated rising prices for hospital stays, physician visits, and pharmaceuticals put upward stress on premiums. Blue Shield has created a new initiative that he stated is designed to decrease drug costs and go on financial savings to shoppers.

Even at California corporations providing insurance coverage, the share of workers enrolled in plans with a deductible has roughly doubled in 20 years, rising to 77%, federal knowledge exhibits. Deductibles are the quantity a employee should pay for many forms of care earlier than their insurance coverage firm begins paying a part of the invoice. The common annual deductible for an employer-provided household medical health insurance plan was about $3,200 in 2023.

During the final twenty years, the price of medical health insurance premiums and deductibles in California rose from about 4% of median family revenue to about 12%, in keeping with the UC Berkeley Labor Center, which conducts analysis on labor and employment points.

As a outcome, the middle discovered, many Californians are selecting to delay or forgo well being care, together with some preventive care.

California is attempting to decrease well being care prices by setting statewide spending growth caps, which state officers hope will curb premium will increase. The state just lately established the Office of Health Care Affordability, which set a five-year goal for annual spending progress at 3.5%, dropping to three% by 2029. Failure to hit targets may end in hefty fines for well being care organizations, although that doubtless wouldn’t occur till 2030 or later.

Other states that imposed related caps noticed well being care prices rise extra slowly than states that didn’t, Dietz stated.

“Does that mean that health care becomes affordable for people?” she requested. “No. It means it doesn’t get worse as quickly.”

This article was produced by KFF Health News, which publishes California Healthline, an editorially unbiased service of the California Health Care Foundation.

KFF Health News is a nationwide newsroom that produces in-depth journalism about well being points and is likely one of the core working applications at KFF—an unbiased supply of well being coverage analysis, polling, and journalism. Learn extra about KFF.

USE OUR CONTENT

This story may be republished without spending a dime (details).