In his wide-ranging State of the Union handle, President Donald Trump returned to a favourite theme: the price of medical health insurance.

[khn_slabs slabs=”1050860″ view=”inline” /]

In his wide-ranging State of the Union handle, President Donald Trump returned to a favourite theme: the price of medical health insurance.

[partner-box]He cited the excessive price of premiums for individuals who purchase their protection by the Affordable Care Act marketplaces and mentioned his administration has offered new, more cost effective protection.

“I moved quickly to provide affordable alternatives. Our new plans are up to 60% less expensive and better,” Trump advised the lawmakers gathered on the Capitol.

So we puzzled, to which new options was he referring? We reached out to the White House to ask.

Spokesperson Adam Kennedy responded that the president was speaking about short-term, limited-duration plans. But that received us considering: Are they actually inexpensive and higher? Or merely higher than nothing?

First, Are They New?

They are usually not. As background, short-term insurance coverage have been round for many years in varied iterations and are usually thought-about a stopgap resolution for folks between jobs or attending faculty. They present some protections, normally paying a share of hospital and physician payments after the policyholder meets a deductible.

But they’ve all the time been a bit controversial.

Unlike the ACA plans now out there, short-term plans can bar folks with well being situations from enrolling or exclude protection for particular situations or remedies. They additionally provide fewer advantages — which means they aren’t required to adjust to the well being legislation’s mandated important advantages requirement.

[khn_slabs slabs=”790331″ view=”inline” /]

So, for instance, they don’t must cowl pharmaceuticals, or psychological well being providers or substance abuse therapy — and lots of don’t. In addition, they’ll set annual or lifetime caps on advantages. Almost all exclude maternity care.

If an individual develops a well being situation in the course of the protection time period, insurers can look by their medical data and, in some instances, retroactively cancel the plans — or refuse to resume the protection on the finish of the coverage’s time period.

The Obama administration restricted these insurance policies, which nonetheless can’t be offered on the ACA marketplaces and don’t qualify for subsidies, to a most protection interval of 90 days, down from the 364 days that utilized beforehand.

The Trump administration reversed that time-limit restriction in 2018 and constructed on it by permitting insurers to supply insurance policies renewable for up to three years.

Officials, together with Health and Human Services Secretary Alex Azar, mentioned on the time that these short-term plans present an alternate however aren’t match for everybody.

For occasion, the Trump rules require the insurance policies to hold a warning that they aren’t “required to comply with federal requirements for health insurance.” They additionally state that buyers ought to “check the policy carefully to make sure you understand what the policy does and doesn’t cover.”

Are These Plans Less Expensive?

The White House pointed us towards a January 2019 report produced by the Congressional Budget Office and the Joint Committee on Taxation because the supply for the president’s assertion that these plans are 60% inexpensive.

It shortly turns into clear that the evaluation could be very wonky and complicated.

After all, it’s not simple to undertaking what advantages insurers will embody in short-term plans or what they’ll cost people, which might range primarily based on their well being. Even the analysts referred to as the estimating course of “challenging.”

When it got here proper all the way down to it, they hedged: Short-term plans are probably cheaper than the lowest-cost ACA plan for some shoppers, however dearer for others. For instance, individuals who get a federal tax credit score to purchase ACA-compliant insurance coverage or those that are older or much less wholesome would probably pay extra in premiums for a standard short-term plan, the analysts mentioned.

Conversely, these with out subsidies, particularly youthful or more healthy shoppers, may pay as a lot as 60% lower than they might for the lowest-cost plan by the ACA, the evaluation concluded. Another examine, not cited by the White House however completed by the conservative Manhattan Institute, additionally listed caveats, however extra robustly defended the plans as inexpensive. Premiums for short-term plans are decrease — in some instances, virtually half the fee — of ACA plans, it concluded.

But critics put these worth tags in context. “I don’t have a reason to suspect the 60% is wrong if they’re lining them up against ACA plans, but if you’re a health plan that doesn’t cover much, it’s easy enough to offer a cheap premium,” mentioned Sabrina Corlette, analysis professor and co-director of the Center on Health Insurance Reforms at Georgetown University.

So That Gets To The Question, Are They Better?

The consensus is that the protection short-term plans present isn’t higher than that of ACA plans. But it could possibly be higher than going with out insurance coverage fully.

“Why not throw another option out there?” mentioned Doug Badger, senior fellow on the conservative Galen Institute. “You might say this plan isn’t as good as that plan, but we may both agree that having this one is better than nothing.”

He mentioned that must be a call made by shoppers, who can weigh the professionals and cons: “They know their circumstances and risk tolerance.”.

Still, it’s a bet, as nobody is aware of what well being situations may befall them. A plan that doesn’t cowl pharmaceuticals could also be high-quality the primary month, but when a critical sickness crops up, it immediately has surprising prices.

Others additionally be aware that short-term plans could have wider networks of medical doctors and hospitals than some ACA plans, giving shoppers extra choices.

“In Texas, for example, you cannot buy an ACA plan that covers MD Anderson,” the most cancers middle of the University of Texas, mentioned Brian Blase, CEO of Blase Policy Strategies. Blase has suggested Trump on his well being coverage efforts. “The only way you can have such a plan that includes MD Anderson — unless you have employer coverage — is in a short-term plan.”

[khn_slabs slabs=”1050864″ view=”pull-right” /]

Again, good to have a large community. But there’s a conundrum. Someone with most cancers — interested in a community as a result of it consists of MD Anderson — could be rejected by most short-term plans.

That potential to reject candidates — or critically restrict protection of their preexisting situations — helps hold premiums down.

But these are additionally the principle causes consultants say the plans are usually not higher than these supplied below the ACA, which bars such limits.

A preexisting situation is commonly outlined as something handled — or for which a “prudent person” ought to have sought therapy — in the course of the earlier 12 months to 5 years, relying on the insurer.

“If you have high blood pressure and, while on one of these plans, you have a heart attack, the plan could say that was a preexisting condition,” mentioned Corlette.

State regulation of such plans varies extensively, as do the protection advantages and limits supplied by varied insurers. Some have limits listed within the high-quality print.

While short-term plans have been embraced by regulators in some states, practically half of all states have moved to restrict them to lower than 12 months. Four — California, Massachusetts, New Jersey and New York — have barred them altogether.

Those states cite issues concerning the impact on ACA premiums and the danger that buyers could possibly be left hanging by the extra restricted nature of the short-term plans.

Our Ruling

Trump mentioned these are new plans which can be 60% cheaper and higher.

But short-terms plans are usually not a brand new concept. Just how less expensive they’re depends upon quite a lot of elements, consultants advised us. And it’s very laborious to look at them in an apples-to-apples comparability with ACA plans, which cowl much more and are required to simply accept all candidates.

Given the constraints of short-term plans, they’re not higher than ACA plans for most individuals, as a result of policyholders might face doubtlessly important monetary threat — or discover their therapy wants are usually not coated. They’re undoubtedly not higher for individuals who qualify for federal subsidies to purchase ACA insurance coverage, particularly these on the decrease finish of that earnings vary, the place the subsidies are bigger.

That mentioned, a short-term plan could also be higher than going with out protection in any respect, notably for a younger or in any other case wholesome individual, whose earnings is above subsidy limits.

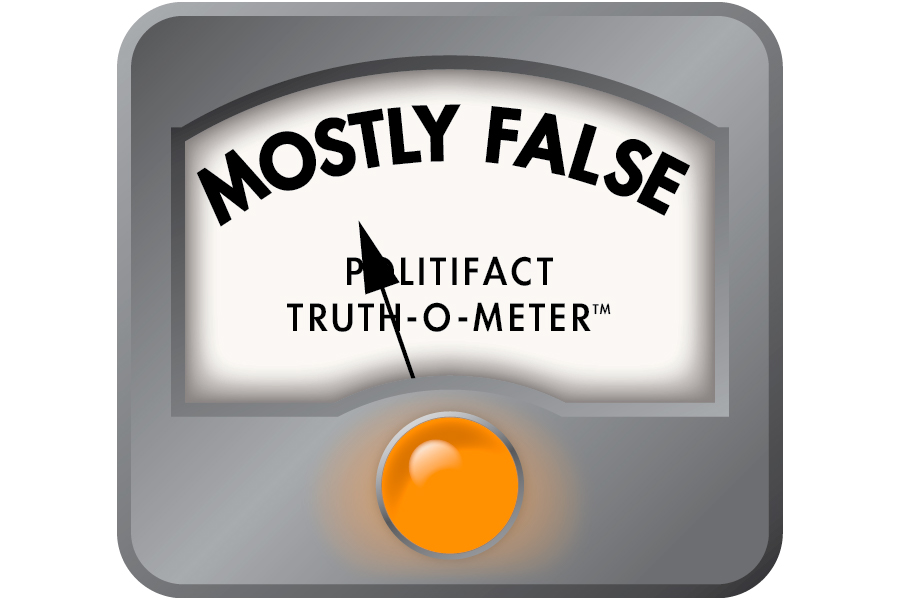

We price this declare as Mostly False.

This story could be republished without cost (details). He cited the excessive price of premiums for individuals who purchase their protection by the Affordable Care Act marketplaces and mentioned his administration has offered new, more cost effective protection.

“I moved quickly to provide affordable alternatives. Our new plans are up to 60% less expensive and better,” Trump advised the lawmakers gathered on the Capitol.

So we puzzled, to which new options was he referring? We reached out to the White House to ask.

Spokesperson Adam Kennedy responded that the president was speaking about short-term, limited-duration plans. But that received us considering: Are they actually inexpensive and higher? Or merely higher than nothing?

First, Are They New?

They are usually not. As background, short-term insurance coverage have been round for many years in varied iterations and are usually thought-about a stopgap resolution for folks between jobs or attending faculty. They present some protections, normally paying a share of hospital and physician payments after the policyholder meets a deductible.

But they’ve all the time been a bit controversial.

Unlike the ACA plans now out there, short-term plans can bar folks with well being situations from enrolling or exclude protection for particular situations or remedies. They additionally provide fewer advantages — which means they aren’t required to adjust to the well being legislation’s mandated important advantages requirement.

So, for instance, they don’t must cowl pharmaceuticals, or psychological well being providers or substance abuse therapy — and lots of don’t. In addition, they’ll set annual or lifetime caps on advantages. Almost all exclude maternity care.

If an individual develops a well being situation in the course of the protection time period, insurers can look by their medical data and, in some instances, retroactively cancel the plans — or refuse to resume the protection on the finish of the coverage’s time period.

The Obama administration restricted these insurance policies, which nonetheless can’t be offered on the ACA marketplaces and don’t qualify for subsidies, to a most protection interval of 90 days, down from the 364 days that utilized beforehand.

The Trump administration reversed that time-limit restriction in 2018 and constructed on it by permitting insurers to supply insurance policies renewable for up to three years.

Officials, together with Health and Human Services Secretary Alex Azar, mentioned on the time that these short-term plans present an alternate however aren’t match for everybody.

For occasion, the Trump rules require the insurance policies to hold a warning that they aren’t “required to comply with federal requirements for health insurance.” They additionally state that buyers ought to “check the policy carefully to make sure you understand what the policy does and doesn’t cover.”

Are These Plans Less Expensive?

The White House pointed us towards a January 2019 report produced by the Congressional Budget Office and the Joint Committee on Taxation because the supply for the president’s assertion that these plans are 60% inexpensive.

It shortly turns into clear that the evaluation could be very wonky and complicated.

After all, it’s not simple to undertaking what advantages insurers will embody in short-term plans or what they’ll cost people, which might range primarily based on their well being. Even the analysts referred to as the estimating course of “challenging.”

When it got here proper all the way down to it, they hedged: Short-term plans are probably cheaper than the lowest-cost ACA plan for some shoppers, however dearer for others. For instance, individuals who get a federal tax credit score to purchase ACA-compliant insurance coverage or those that are older or much less wholesome would probably pay extra in premiums for a standard short-term plan, the analysts mentioned.

Conversely, these with out subsidies, particularly youthful or more healthy shoppers, may pay as a lot as 60% lower than they might for the lowest-cost plan by the ACA, the evaluation concluded. Another examine, not cited by the White House however completed by the conservative Manhattan Institute, additionally listed caveats, however extra robustly defended the plans as inexpensive. Premiums for short-term plans are decrease — in some instances, virtually half the fee — of ACA plans, it concluded.

But critics put these worth tags in context. “I don’t have a reason to suspect the 60% is wrong if they’re lining them up against ACA plans, but if you’re a health plan that doesn’t cover much, it’s easy enough to offer a cheap premium,” mentioned Sabrina Corlette, analysis professor and co-director of the Center on Health Insurance Reforms at Georgetown University.

So That Gets To The Question, Are They Better?

The consensus is that the protection short-term plans present isn’t higher than that of ACA plans. But it could possibly be higher than going with out insurance coverage fully.

“Why not throw another option out there?” mentioned Doug Badger, senior fellow on the conservative Galen Institute. “You might say this plan isn’t as good as that plan, but we may both agree that having this one is better than nothing.”

He mentioned that must be a call made by shoppers, who can weigh the professionals and cons: “They know their circumstances and risk tolerance.”.

Still, it’s a bet, as nobody is aware of what well being situations may befall them. A plan that doesn’t cowl pharmaceuticals could also be high-quality the primary month, but when a critical sickness crops up, it immediately has surprising prices.

Others additionally be aware that short-term plans could have wider networks of medical doctors and hospitals than some ACA plans, giving shoppers extra choices.

“In Texas, for example, you cannot buy an ACA plan that covers MD Anderson,” the most cancers middle of the University of Texas, mentioned Brian Blase, CEO of Blase Policy Strategies. Blase has suggested Trump on his well being coverage efforts. “The only way you can have such a plan that includes MD Anderson — unless you have employer coverage — is in a short-term plan.”

Again, good to have a large community. But there’s a conundrum. Someone with most cancers — interested in a community as a result of it consists of MD Anderson — could be rejected by most short-term plans.

That potential to reject candidates — or critically restrict protection of their preexisting situations — helps hold premiums down.

But these are additionally the principle causes consultants say the plans are usually not higher than these supplied below the ACA, which bars such limits.

A preexisting situation is commonly outlined as something handled — or for which a “prudent person” ought to have sought therapy — in the course of the earlier 12 months to 5 years, relying on the insurer.

“If you have high blood pressure and, while on one of these plans, you have a heart attack, the plan could say that was a preexisting condition,” mentioned Corlette.

State regulation of such plans varies extensively, as do the protection advantages and limits supplied by varied insurers. Some have limits listed within the high-quality print.

While short-term plans have been embraced by regulators in some states, practically half of all states have moved to restrict them to lower than 12 months. Four — California, Massachusetts, New Jersey and New York — have barred them altogether.

Those states cite issues concerning the impact on ACA premiums and the danger that buyers could possibly be left hanging by the extra restricted nature of the short-term plans.

Our Ruling

Trump mentioned these are new plans which can be 60% cheaper and higher.

But short-terms plans are usually not a brand new concept. Just how less expensive they’re depends upon quite a lot of elements, consultants advised us. And it’s very laborious to look at them in an apples-to-apples comparability with ACA plans, which cowl much more and are required to simply accept all candidates.

Given the constraints of short-term plans, they’re not higher than ACA plans for most individuals, as a result of policyholders might face doubtlessly important monetary threat — or discover their therapy wants are usually not coated. They’re undoubtedly not higher for individuals who qualify for federal subsidies to purchase ACA insurance coverage, particularly these on the decrease finish of that earnings vary, the place the subsidies are bigger.

That mentioned, a short-term plan could also be higher than going with out protection in any respect, notably for a younger or in any other case wholesome individual, whose earnings is above subsidy limits.

We price this declare as Mostly False.